Three predictions for power development in 2026

By: James McWalter

2025 was the year that everyone started paying attention to energy.

Before then, stories that would blow up among us energy nerds stayed in our own curated spaces. Now? The average American is tracking electricity prices, data center construction plans, and talking about how AI is reshaping everyday life.

The money flowing into energy infrastructure tells the story. Utilities are projected to spend $1.4T over the next 5 years to meet AI demand, double what we spent in the previous decade. We went from flat load growth for 10 years to projections of 25% growth over the next 5 years. That's not a trend line. That's a break.

Those of us working in energy infrastructure had to stay agile through 2025. Policy changes came fast: the One Big Beautiful Bill Act, Texas reining in large loads with new transmission fees and interconnection requirements, Maryland standardizing solar siting and expanding transmission corridors. Across the Southeast, states experimented with incentives and grid impact studies for data centers. Hyperscaler investment announcements dropped daily. It was intense.

As we head into 2026, I’ve had time to reflect on the madness and ask myself a simple question: what will actually look different next year?

Not incrementally different, but structurally different.

Here are three predictions I feel strongly about, based on what we’re seeing across power development, data centers, and policy. None of these are about shiny new technologies. They’re about operating reality.

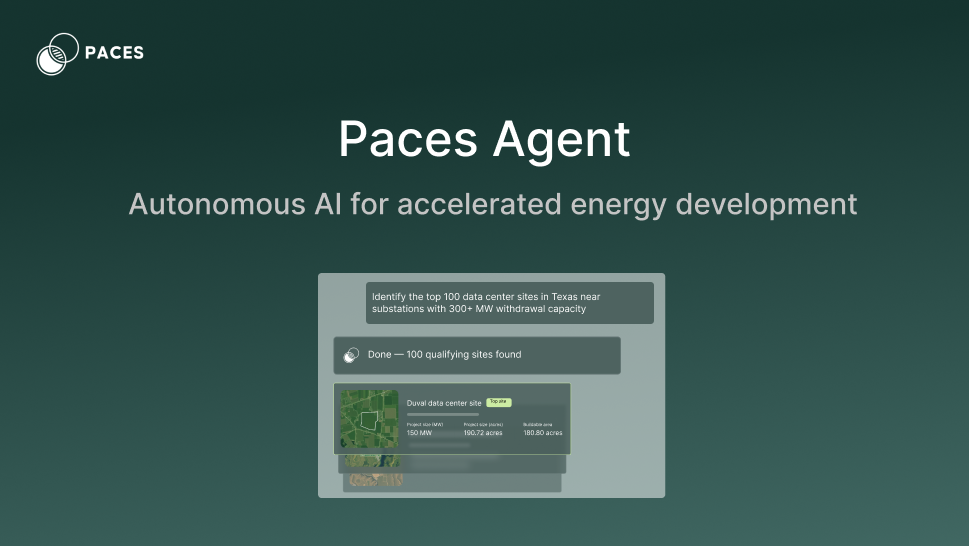

1) Energy development will reset its cost structure permanently

In 2026, the best power developers will have larger pipelines while having lean teams. The golden rule for developers used to be 100 people/GW. In September, I wrote about how I believe that by 2030 we’ll see a one-person, billion-dollar development company. We’re now already seeing dev shops pursuing a lean and alpha-generating development model, with a goal of generating hundreds of MWs with a team of 10 or fewer.

Large developers, especially those active in M&A, will be running 30–60% lower SG&A per MW than 2025. Not just through the layoffs we’ve been seeing, but by replacing manual work with software and AI across siting, screening, permitting prep, and diligence.

Headcount growth will decouple from MW growth. Tech spend will replace junior labor. The operating model shifts from “more people, more projects” to “better systems, faster decisions.”

This isn’t optional. Developers that fail to retool and embed AI and software as a core operating leverage will become structurally uncompetitive on both speed and returns. Infrastructure and private equity don’t want to invest in more people, they want to invest in hard assets. And in a market where delays directly destroy IRR, operational leverage is the real moat.

This is the new era for power development. The firms adopting it in 2026 will be the ones setting the pace this year.

2) Data center growth will split, creating a true middle tier

Hyperscale campuses aren’t going away, but they’re getting harder to build.

Grid congestion and time-to-power constraints will push a meaningful share of growth toward 50–100 MW modular campuses in 2026. These aren’t true “edge” sites, and they’re not gigawatt mega-sites either.

Think of them as a new middle tier between hyperscaler and edge sites:

- Located near available generation, substations, or behind-the-meter assets

- Designed for speed, redundancy, and phased expansion

- Optimized for certainty, not maximum scale

As hyperscalers become rarer, these sub-100 MW deployments will absorb demand that can’t afford to wait. The winners will be operators who can model power pathways creatively and execute in parallel.

3) Permitting reform will help, but only the prepared

Yes, permitting reform is coming. And yes, it will shorten timelines for a subset of projects.

But in 2026, the benefits will be highly uneven.

For the last year, permitting reform has been stuck in a familiar loop: big promises in Congress, stalled grand bargains, and a steady drip of narrower NEPA and agency tweaks that quietly change the rules for a subset of projects. Median federal review times are still measured in years, but there are now real, faster lanes for projects that fit the new criteria.

Recent reforms have focused on tightening NEPA timelines, expanding categorical exclusions for clearly low‑impact activities, and standardizing how agencies decide what level of review a project needs. Late‑2025 moves like the SPEED Act in the House, along with updated NEPA procedures at key agencies, point toward 2026 being the first year those changes start to show up in actual project schedules.

Projects that arrive with pre‑screened, low‑conflict sites and clean documentation are the ones that can plausibly slot into these streamlined tracks and capture most of the upside. Everyone else will keep feeling like nothing has changed, because the underlying coordination problems, litigation risks, and local constraints have not gone away.

Reform doesn’t eliminate permitting work; it front‑loads it. In 2026, preparedness, and specifically how quickly you can be prepared, not policy alone, will determine who actually ships projects faster.

The common thread

The through line here isn't just about speed. It's about changing the operating model before the market forces you to.

The developers who thrive in 2026 won't be the ones with the biggest teams or the deepest Rolodexes. They'll be the ones who rebuilt their workflows around better systems and use automation to build more MWs with leaner teams, find clear pathways to power, and are prepared to move on permitting reforms.

We're building Paces to be the backbone of this operating model.

If you agree or disagree with my takes, feel free to reach out on LinkedIn. I'm genuinely curious where others see this heading.

If you’re interested in how Paces is addressing some of these predictions or how they map to your pipeline, book some time with our team.

The next year will be decisive.

Sign up for emails

Find the right sites faster, assess feasibility with world class data, and track progress across your entire project pipeline with software built to compress your workflow.